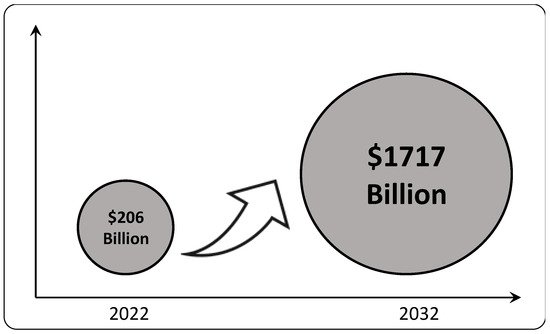

Global electric vehicle (EV) sales rose 23% year-on-year in October, underscoring a decisive shift in the world’s auto and technology supply chains. The surge is creating new winners in battery, semiconductor, and materials sectors while exposing vulnerabilities among traditional automakers and suppliers that have lagged in electrification.

The main keyword “EV sales growth” highlights a key inflection point for global manufacturing and trade. As adoption accelerates across major markets — particularly China, the US, and Europe — supply chains are being reconfigured around battery metals, software-driven mobility, and regional production hubs that prioritize resilience over scale.

EV demand reshapes global manufacturing landscape

October’s 23% increase in global EV sales marks one of the strongest growth months in 2025, with total volumes nearing 1.5 million units for the month, according to data compiled by EV-Volumes and BloombergNEF. China accounted for more than half of total sales, led by BYD, Geely, and Tesla’s Shanghai Gigafactory output. Europe contributed roughly 25% of sales, while North America captured close to 15%, showing signs of renewed demand following tax incentive extensions under the US Inflation Reduction Act.

The data reinforces a clear trajectory: electric mobility is no longer a niche segment but a core component of global industrial strategy. However, the rapid expansion is redrawing the competitive map across the auto value chain. Companies leading in batteries, software integration, and component miniaturization are gaining ground, while legacy OEMs with slower electrification timelines face margin compression and supply bottlenecks.

Battery and semiconductor suppliers emerge as key winners

The surge in EV sales has fueled parallel growth in battery demand, particularly for lithium iron phosphate (LFP) and nickel-manganese-cobalt (NMC) chemistries. Chinese giants CATL and BYD together supplied nearly 50% of global EV batteries in October, while South Korea’s LG Energy Solution and Samsung SDI maintained strong momentum in premium markets.

Battery component shortages are easing, but supply chain concentration remains a strategic risk. The industry’s dependency on China for more than 70% of cathode materials and rare earth processing continues to drive policy responses from the US and EU, both of which are accelerating domestic production under green industrial frameworks.

Meanwhile, semiconductor suppliers are benefiting from the growing compute demands of EVs. Vehicles now incorporate more chips than ever before — not only for core control systems but also for autonomous driving, connectivity, and infotainment. Qualcomm, Nvidia, and Renesas have secured major design wins in next-generation EV platforms, while traditional automotive chipmakers like NXP and Infineon are retooling product lines for high-efficiency computing and power management.

Traditional automakers face mixed fortunes

Legacy automakers’ performance in October highlighted the growing divergence within the sector. Tesla’s global deliveries rebounded 18% after production slowdowns in Q3, while China’s BYD hit a record high of 326,000 monthly units, surpassing its Western rivals in total volume.

In contrast, traditional carmakers like Volkswagen, Toyota, and Stellantis are grappling with slower EV ramp-ups. Supply chain constraints, higher battery costs, and lower consumer subsidies in Europe have pressured margins. Volkswagen recently cut EV output targets for 2025, citing subdued demand in its key markets.

Japanese automakers, long resistant to full electrification, are accelerating hybrid strategies instead. Toyota and Honda are betting on solid-state battery development for post-2027 launches, but analysts warn that delayed mass-market EV rollout could erode global market share as Chinese and American rivals gain scale.

Supply chain restructuring enters its next phase

The EV boom is accelerating a broader restructuring of global manufacturing networks. Companies are diversifying away from single-country dependencies and building regional ecosystems to mitigate geopolitical risk. The US and EU are incentivizing “friend-shoring” and local assembly of EV batteries and components.

India, Indonesia, and Mexico are emerging as major alternative manufacturing bases. Indonesia’s nickel reserves have made it a magnet for battery investment from Korean and Chinese firms, while Mexico’s proximity to the US market and USMCA trade advantages have attracted automakers such as Tesla and BMW.

Technology convergence is also reshaping how supply chains operate. Software-defined manufacturing, AI-driven logistics, and digital twins are being adopted to increase resilience and cut costs. Analysts expect these structural changes to define the next decade of industrial competitiveness, with national policies increasingly centered on clean tech independence.

Investment, policy, and sustainability implications

Investors are repositioning portfolios to reflect this shift in global manufacturing power. Battery materials, EV semiconductors, and grid infrastructure are among the top-performing sectors in equity markets this quarter. Meanwhile, funds with exposure to traditional auto suppliers and internal combustion engine (ICE) components are under pressure.

For policymakers, the surge in EV adoption underscores the urgency of securing critical minerals, recycling capabilities, and clean energy infrastructure. Governments are also recalibrating trade policy to prevent overdependence on specific geographies for essential inputs.

At the same time, environmental sustainability is under scrutiny. The rapid expansion of EV production has intensified debates over the carbon footprint of mining, battery waste management, and the lifecycle of electric vehicles. Regulators in Europe and Asia are tightening lifecycle emissions standards, forcing manufacturers to adopt cleaner supply chain practices.

Takeaways

- Global EV sales rose 23% in October, with China leading the surge.

- Battery and semiconductor suppliers are the biggest winners in the shifting auto value chain.

- Traditional automakers face competitive and cost pressures amid slower EV transitions.

- Supply chains are regionalizing, with new hubs emerging in India, Indonesia, and Mexico.

FAQs

Q1: What drove the 23% increase in global EV sales in October?

A1: Strong demand in China, new model launches, and stable battery supply chains contributed to the surge, alongside renewed consumer incentives in the US and Europe.

Q2: Which companies are benefiting most from the EV supply chain shift?

A2: Battery producers like CATL, BYD, and LG Energy Solution, as well as semiconductor firms such as Qualcomm and Nvidia, are leading beneficiaries of the transition.

Q3: How are traditional automakers responding to the competition?

A3: Some are focusing on hybrid and solid-state battery technology, while others are cutting costs and partnerships to accelerate EV timelines, though challenges remain.

Q4: What are the biggest risks in the global EV supply chain?

A4: Overconcentration of material processing in China, limited critical mineral supply, and high capital requirements for new production hubs pose key vulnerabilities.